Coronavirus: is the market’s reaction overblown?

Action to contain the new coronavirus, involving travel restrictions and quarantine areas, is economically damaging. Recent falls in stock market reflect this.

We do not have full details of the disease and its severity but it is becoming increasingly clear that it is most dangerous to the elderly and infirm. Unusually, young children do not appear to be particularly susceptible and reported infections among the young appear surprisingly low. We have no wish to dismiss the human tragedy involved, but the groups most at threat are largely economically inactive. Health care services will come under pressure and care costs will be high, however, this burden will largely fall on the public sector. Taxes could consequently rise or, more likely, public borrowing will increase.

Global central banks have cut interest rates to support the economy. This should help offset the damage wrought to supply chains and demand. Economists’ estimates of the costs of the virus range anywhere between 0.5% and 10% of GDP depending upon its severity, with the central projections appearing to be falling around 2%. The economic costs of closing schools are significant, as parents become obliged to stop work to care for their children. If the young are largely unaffected and presumably not part of the virus’s transmission route, schools may not have to close. This will help to reduce the economic implications.

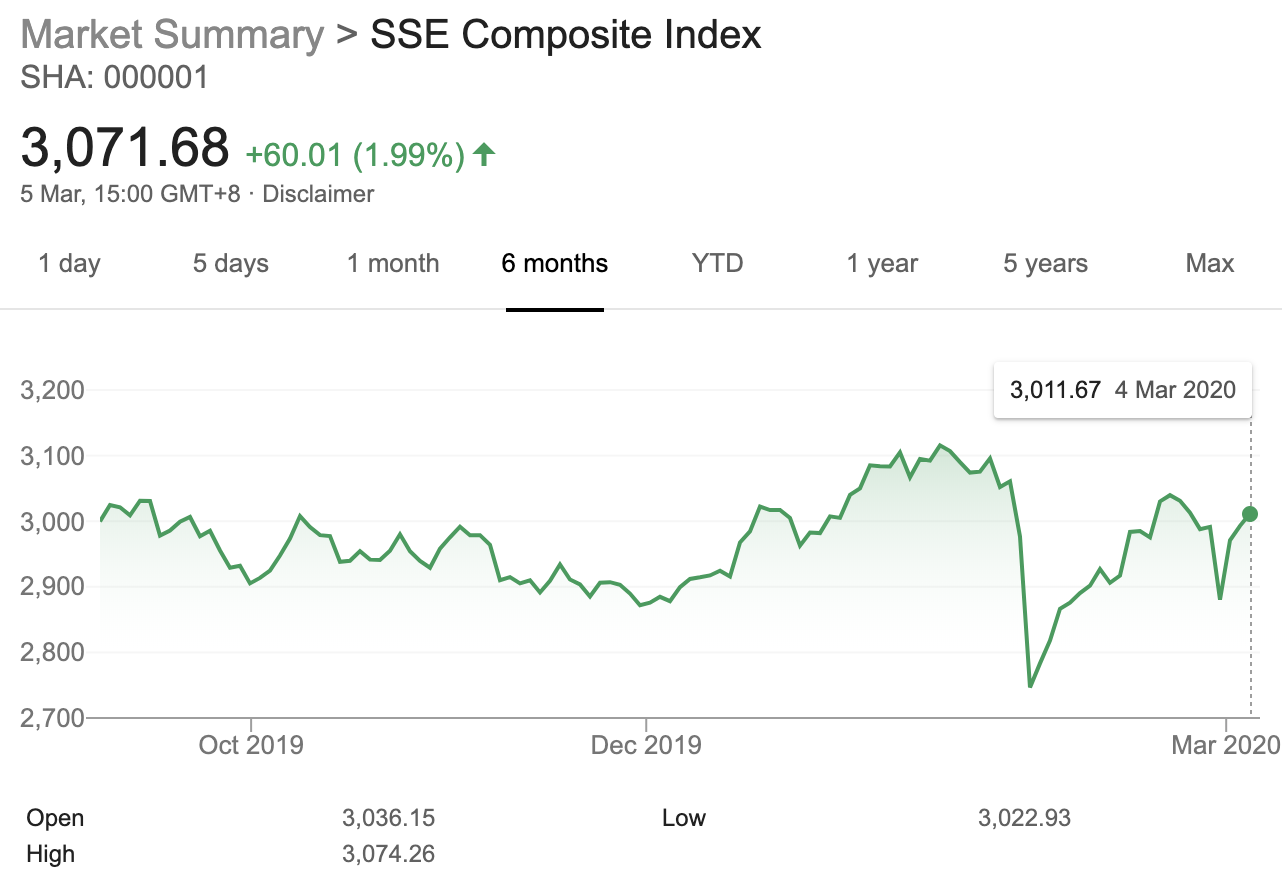

The impact on the stock market may be short term in nature and a 'V' shaped recovery in markets is not out of the question. Indeed, this seems to be the path that the Chinese stock market is taking.

Source: Google Finance, 2020

If countermeasures against the virus, such as wide scale quarantine measures and stringent travel restrictions, are in place for an extended period, the impact on commerce is likely to be more pronounced. Then, expectations of a 'U' or 'L' shaped recovery in markets may be more appropriate. At this juncture it is too early to tell.

As at 5th March 2020.

We do not have full details of the disease and its severity but it is becoming increasingly clear that it is most dangerous to the elderly and infirm. Unusually, young children do not appear to be particularly susceptible and reported infections among the young appear surprisingly low. We have no wish to dismiss the human tragedy involved, but the groups most at threat are largely economically inactive. Health care services will come under pressure and care costs will be high, however, this burden will largely fall on the public sector. Taxes could consequently rise or, more likely, public borrowing will increase.

Global central banks have cut interest rates to support the economy. This should help offset the damage wrought to supply chains and demand. Economists’ estimates of the costs of the virus range anywhere between 0.5% and 10% of GDP depending upon its severity, with the central projections appearing to be falling around 2%. The economic costs of closing schools are significant, as parents become obliged to stop work to care for their children. If the young are largely unaffected and presumably not part of the virus’s transmission route, schools may not have to close. This will help to reduce the economic implications.

The impact on the stock market may be short term in nature and a 'V' shaped recovery in markets is not out of the question. Indeed, this seems to be the path that the Chinese stock market is taking.

Source: Google Finance, 2020

If countermeasures against the virus, such as wide scale quarantine measures and stringent travel restrictions, are in place for an extended period, the impact on commerce is likely to be more pronounced. Then, expectations of a 'U' or 'L' shaped recovery in markets may be more appropriate. At this juncture it is too early to tell.

As at 5th March 2020.