By Jasmine Yeo Ruffer LLP - Investment Manager

The Bank of Japan has signalled the beginning of the end of its ultra-loose policy stance. The yen’s response has been muted – so far.

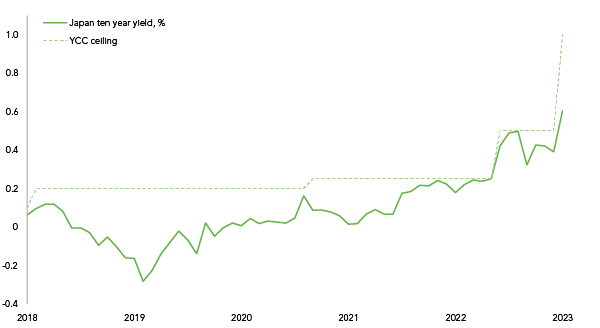

The Ten Year Yield versus Yield Curve Control (YCC) ceiling

Chart source: FactSet, Bank of Japan, Ruffer analysis, data to July 2023

The Bank of Japan (BoJ) – longtime poster child of ultra-loose monetary policy – looks to have finally started relaxing its grip on bond yields. In the dog days of summer, Japan’s central bankers announced a shift to ‘flexible yield curve control’. The yield on ten year Japanese government bonds (JGBs) will now be managed with an upper limit of 1% (double the level last reset in December). This month’s chart shows the step change to the BoJ’s cap and the corresponding moves in the ten year yield.

A 0.5 percentage point increase to the upper limit on a ten year yield doesn’t sound particularly groundbreaking. More of a snip than a snap. The yen’s initial reaction was muted too – rising 2% against the dollar on the day before sliding back to below pre-announcement levels.

This is mainly because there has been no let-up in the popular yen carry trade – whereby investors borrow yen to buy dollars and then harvest the higher yield. As rates have risen in the US over the summer months, this trade has continued to be a simple, mechanical and rewarding source of returns.

But the contestants’ fingers are on the buzzers. This policy adjustment matters because it changes a key dynamic in global debt markets.

Historically, when JGB yields float higher, domestic investors are incentivised to unwind their foreign bond holdings and repatriate the proceeds back into the home market. The dynamic is more pronounced today due to how far Japan’s monetary policy has diverged from other major central banks – not least the US Federal Reserve, which has conducted a fast and steep hiking cycle to contain inflation. Given Japanese government debt represents 16% of global sovereign bond indexes, an eastbound flow of capital could send ripples across markets. Most patently it would revive a flagging yen.

Whilst the event risk (‘what will happen if the BoJ removes the cap?’) has been allayed, the pressure on yields could gradually drive global risk premia back up and further expose market vulnerabilities. We think this is just the first step on a longer path to a stronger yen and higher Japanese rates.

Moreover, the BoJ is conditioning its inflation outlook on further US disinflation and economic slowdown. If US inflation proves stickier than expected, the BoJ’s revised stance may amplify the market’s response.

Markets are currently pricing in a lot of good news: immaculate disinflation, a recessionary ‘near-miss’ and rampant investor appetite for US equity and corporate debt. But disappointment on any of those three fronts would force a rethink.

Defensive assets have been punished by markets this year, as animal spirits have been unleashed. But we have high conviction that the yen is exactly the sort of asset to which investors will flock as the effects of tighter financial conditions come to bear.

Click here for the original article. If you would like to receive Ruffer’s monthly Green Line directly to your inbox please subscribe here. For more information on the A-rated WS Ruffer Diversified Return fund here.

***

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This article does not take account of any potential investor’s investment objectives, particular needs or financial situation. This article reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. This article is issued by Ruffer LLP which is authorised and regulated by the Financial Conduct Authority in the UK and is registered as an investment adviser with the US Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training. © Ruffer LLP 2023. Registered in England with partnership No OC305288. 80 Victoria Street, London SW1E 5JL. For US institutional investors: securities offered through Ruffer LLC, Member FINRA. Ruffer LLC is doing business as Ruffer North America LLC in New York. Read the disclaimer